More ways to use your Cashback Credit Card

Everyday Purchases

Use your cashback credit card for regular expenses like groceries, gas, and utilities. Most cards offer 1–5% cashback on these categories, which adds up over time.

Big-Ticket Purchases

For larger purchases, such as electronics or appliances, using a cashback credit card allows you to earn rewards while covering significant costs.

Online Shopping

Many cashback cards offer bonus rewards for online shopping, especially if you shop through their associated portals or at select retailers.

Travel and Dining

Many cards offer higher cashback rates for travel-related expenses like flights, hotels, and car rentals, as well as dining out. This can help you save on vacations or frequent business trips.

Bill Payments

Paying monthly bills such as subscriptions, insurance premiums, or even taxes with a cashback credit card can earn you cashback while keeping your bills on track. Just be mindful of potential processing fees for some bill payments.

Get cashback credit card from 3 simple process

Obtaining a cashback credit card is usually a simple process that can be broken down into three easy steps:

Research and compare

Submit an application

Approval and activation

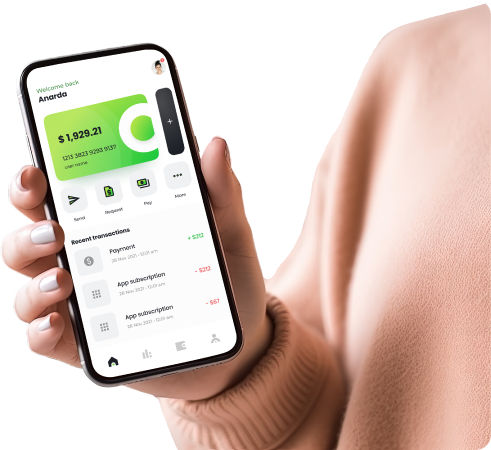

No overdraft Fees

Do all your banking safely and conveniently through our mobile app